You bought or refinanced your Hoboken home when mortgage rates hovered near 3% — and now, every instinct says, “Don’t lose that rate.”

But life has changed. Maybe you’ve built a family, your kids are in school, and that once-perfect space is starting to feel tight. You’re craving more room — an extra bedroom, home office, basement play area, or outdoor space. Yet new homes across Hoboken, Jersey City, or Weehawken come with higher prices and 6%+ mortgage rates.

So the big question is:

Is it ever smart to sell a 3% home to buy at 6%?

Let’s explore this from a local, data-driven, and lifestyle-focused perspective.

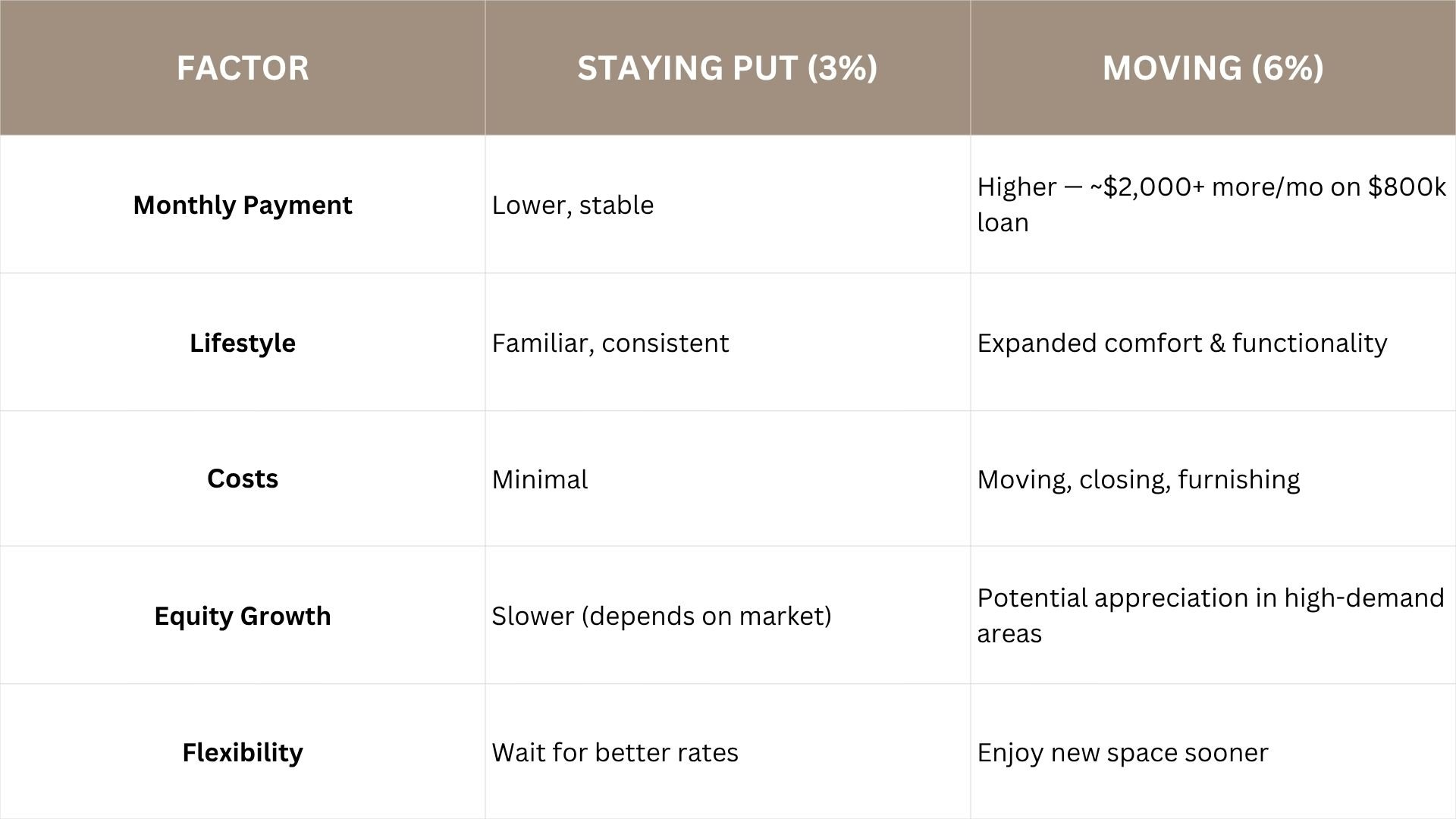

Should You Stay Put in Your Hoboken Home with a 3% Mortgage?

1. You’re Sitting on “Golden Handcuffs” — in a Good Way

A 3% mortgage is a rare asset in 2025. With average 30-year fixed rates around 6.27% (FRED data, Oct 2025), your financing costs are nearly half that of a new loan.

For the same $800,000 balance, you’d pay roughly $2,000/month in interest at 3%, versus $4,000/month at 6%. That’s $24,000 in annual savings — real money staying in your pocket.

2. The Power of Stability

If your kids are thriving in school, your routines are set, and your favorite Hoboken cafés and parks are nearby, that stability carries financial and emotional value. Keeping your low-rate home often means keeping your community rhythm intact.

3. Renovate or Reimagine Your Space

Before selling, explore creative ways to make your current space work harder:

-

Add built-ins or clever storage

-

Combine with an adjacent unit (common in Hoboken brownstones)

-

Reconfigure or renovate — often cheaper than trading into a 6%+ mortgage

4. The Option to Wait

If your family can stretch in your current space for another year or two, patience may pay off. Many analysts expect mortgage rates to moderate as inflation cools into 2026. Waiting could mean upgrading and keeping a friendlier rate.

Why Selling and Buying at 6% May Still Make Sense in Hudson County

1. Space Equals Sanity

A bigger home isn’t just square footage — it’s quality of life. If you’re working remotely or your kids need more room, an extra bedroom, yard, or terrace can transform your daily experience.

Sometimes, the cost of comfort outweighs the savings of a low rate.

2. Think Long-Term, Not Month-to-Month

If you plan to stay 10–15 years, a higher rate hurts less over time. You’ll enjoy your ideal space during the years that matter most — while your family is growing.

And when rates drop? You can always refinance.

3. The Equity Upside

Hudson County neighborhoods like Uptown Hoboken, The Heights, and Weehawken Waterfront continue to appreciate thanks to limited inventory and strong demand.

Even at a higher rate, equity growth can offset the short-term cost difference.

4. Lifestyle Alignment

If your dream home offers the kitchen, terrace, or backyard that fits your family’s lifestyle, that intangible value can be priceless. The right space doesn’t just change where you live — it changes how you live.

Smart Framework for Hoboken Homeowners

-

How urgently do we need more space?

-

Could we find better value in nearby towns like Jersey City Heights, Union City, or Westfield?

-

Would remodeling achieve 70–80% of what we want for less?

-

What’s our time horizon — three years, or twenty?

Brian’s Realtor Lens: A Hoboken Reality Check

As a longtime Hoboken agent and resident, I’ve seen both sides of this decision — and lived it myself.

If your next home is truly exceptional — larger, better features, top school district, and a place you’ll stay for a decade or more — it’s worth the higher rate. Over time, lifestyle wins, and refinancing later smooths the financial edge.

After all, how long does it make sense to delay a major improvement in your family’s lifestyle?

But if the price jump feels steep for only modest gains (like one extra bedroom in the same building), consider holding tight. Leverage your low rate, improve where you can, and watch for new inventory or opportunities just outside Hoboken’s core.

Remember: the goal isn’t just to move — it’s to move smarter.

FAQ: Selling with a Low Mortgage Rate

1. Is it smart to sell a home with a 3% mortgage rate?

It depends on your lifestyle needs and time horizon. If your next home will serve you long-term, lifestyle and equity gains may outweigh the rate gap.

2. Will mortgage rates drop in 2026?

Analysts predict gradual moderation as inflation cools, but no one can time the market perfectly — plan based on life, not speculation.

3. What’s the average home price in Hoboken right now?

As of Fall 2025, Hoboken’s median home price hovers around $875,000–$1.2M, depending on location and property type.

Considering Your Next Move?

Thinking about your next chapter in Hoboken or Hudson County?

Let’s talk strategy — not just about rates, but about what truly adds value for your family.